The Deep Value Week – 2025/15

A Few New Write-ups, Discussions on X & a Few Insider Transactions

Companies mentioned:

· Alico (ALCO) – Write-up on TheTigersPrey

· Art's Way Manufacturing (ARTW) - Reports Narrowed Losses as Modular Building Segment Offsets Ag Market Weakness & Insider Purchase

· Chicago Rivet & Machine (CVR) – Mentioned on X

· Deswell Industries (DSWL) & Tandy Leather Factory (TLF) – On Franco Gianotti

· Fonar (FONR) – Mentioned on X

· Key Tronic Corp (KTCC) – Jerome on the Co’s US Focus

· Nacco Industries (NC) - Publishes Investor Update with 2024 Results and Strategic Outlook

· Orbit Garant Drilling (OGD) – New Presentation

· Seneca Foods (SENEA) – Mentioned at Alluvial

· Unifi (UFI) - Launches Biodegradable REPREVE with CiCLO Technology to Combat Microplastic Pollution

· Village Super Market (VLGEA) - Director Kevin Begley Sells 3,000 Shares

· Manitowoc (MTW) - Files U.S. Anti-Dumping Petition Against Japanese Crane Imports

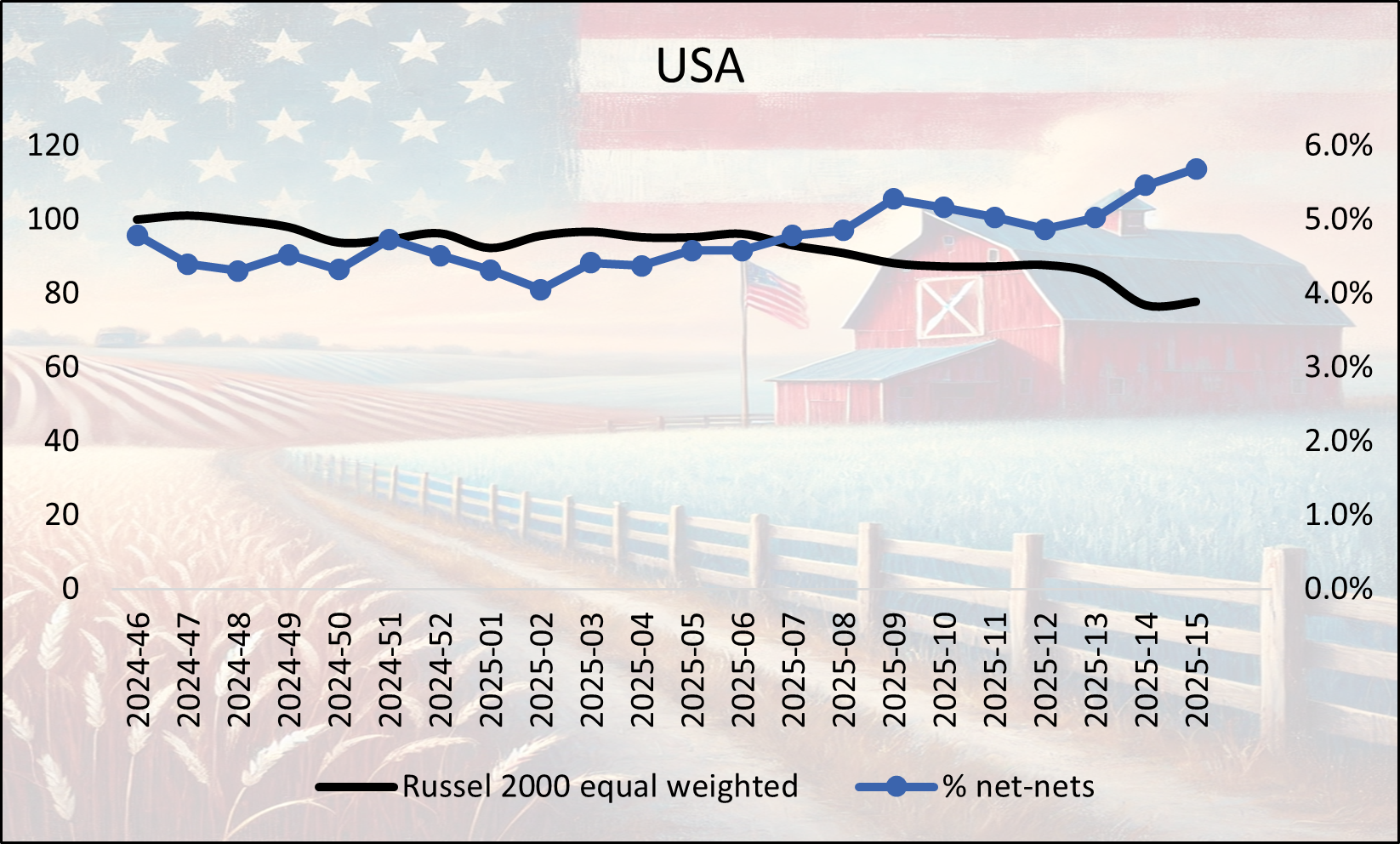

“Graham’s Geiger counter”

Benjamin Graham suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive. Today’s net-nets, however, are not the same as Graham’s net-nets. Many are un-investable being Chinese RTO’s, loss-making biopharma’s etc. But we do think it is interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable. Below is a net-net screen from Stockopedia.

Alico (ALCO) – Write-up on TheTigersPrey

P/TB 0.92 │ URL

Can be read here.

Art's Way Manufacturing (ARTW) - Reports Narrowed Losses as Modular Building Segment Offsets Ag Market Weakness & Insider Purchase

Art’s Way Manufacturing Co., Inc. reported a 10.2% year-over-year revenue decline in Q1 2025 to $5.1m, primarily due to a 30.4% drop in agricultural products sales caused by continued weakness in the ag market. Despite this, the company reduced operating expenses by 19.4% and narrowed its net loss to $56k (vs. $424k loss in Q1 2024). The modular buildings segment saw strong performance, with sales increasing 47.5% to $2.2m and net income improving to $291k, driven by a healthy backlog and continued demand. While ag sales were impacted by high interest rates, lower commodity prices, and dealer destocking, management believes the market has bottomed and anticipates recovery supported by expected Fed rate cuts. Tariff-related cost pressure remains a risk. Earnings per share improved to a loss of $0.01 (vs. $0.08 loss YoY).

On April 10, 2025, Randall C. Ramsey, a director, acquired 6,800 shares of common stock at a price of $1.50 per share in an open market transaction. Following this purchase, Mr. Ramsey holds a total of 67,709 shares directly.

Chicago Rivet & Machine (CVR) – Mentioned on X

P/TB 0.47 │ URL

See below.

Deswell Industries (DSWL) & Tandy Leather Factory (TLF) – On Franco Gianotti

P/TB 0.35 / 0.43 │ URL

Write-up can be read here.

Fonar (FONR) – Mentioned on X

P/TB 0.49 │ URL

Vysse36 posted about Fonar on X.

Key Tronic Corp (KTCC) – Jerome on the Co’s US Focus

P/TB 0.21 │ URL

Jerome shared his thoughts on X.

Nacco Industries (NC) - Publishes Investor Update with 2024 Results and Strategic Outlook

P/TB 0.68 │ URL

On April 9, 2025, NACCO Industries, Inc. filed a Form 8-K to announce the publication of an updated investor presentation, highlighting financial results for FY2024 and strategic developments. Despite prior-year impairments, the company reported a $33.7m net income in 2024, a significant turnaround from a $39.6m loss in 2023. Adjusted EBITDA more than doubled year-over-year to $59.4m. Strong cash generation from coal mining and a growing minerals management portfolio supported results. Expansion continues across segments, including lithium mining (via Sawtooth Mining), ecological restoration, and energy project development under ReGen Resources.

Orbit Garant Drilling (OGD) – New Presentation

P/TB 0.81 │ URL

Seneca Foods (SENEA) – Mentioned at Alluvial

P/TB 0.96 │ URL

Can be read here.

Unifi (UFI) - Launches Biodegradable REPREVE with CiCLO Technology to Combat Microplastic Pollution

P/TB 0.36 │ URL

On April 14, 2025, UNIFI, Inc. (NYSE: UFI), announced the global launch of REPREVE with CiCLO® technology—biodegradable recycled polyester and nylon. Developed in partnership with Intrinsic Advanced Materials, this new yarn incorporates a patented additive at the fiber level, allowing synthetic fibers to break down more naturally in soil and seawater, addressing the issue of microplastic pollution. The technology maintains the performance and dyeability of traditional synthetics and is compatible with all REPREVE-branded products. Early adopters include brands such as Target, Oakley, and Billabong. UNIFI is showcasing the innovation at the Functional Fabric Fair in Portland, April 14–16, 2025.

Village Super Market (VLGEA) - Director Kevin Begley Sells 3,000 Shares

P/TB 1.18 │ URL

On April 9, 2025, Kevin Begley, a director, sold 3,000 shares of Class A Common Stock at a price of $37.40 per share. Following the transaction, Mr. Begley holds 48,961 shares directly.

Manitowoc (MTW) - Files U.S. Anti-Dumping Petition Against Japanese Crane Imports

P/TB 0.61 │ URL

On April 2025, The Manitowoc Company, Inc. filed an anti-dumping petition with the U.S. International Trade Commission and Department of Commerce, accusing Japanese manufacturers—specifically Kobelco—of predatory pricing on lattice-boom crawler cranes. The company claims these practices have harmed its U.S. operations and calls on the government to take corrective action. CEO Aaron Ravenscroft emphasized the need to protect domestic manufacturing and support U.S. workers. The case may result in tariffs or other trade remedies if the allegations are upheld.

The writer may own shares of the companies mentioned. This communication is for informational purposes only. AI helped us with this. Check important info.

I looked at FONR before and it does look nice at first but the company is only entitled to 51% of the cash flows & revenue from the HMCA business (managing MRIs) although they might reports all of the numbers on their statements. I think thats why it trading at its current valuation.

Franco does it the right way, but I think he should also consider discounting the receivables albeit hopefully not by much. Also property can be worth more in some instances and undervalued on the balance sheet.

I hold two small companies where I believe the latter to be true, but there is heavy insider ownership on both and one has an A,B structure. It’s not Seneca, but I believe that structure doesn’t benefit holders there either. Although the value seems to be finally starting to be recognized there and I encourage everyone to read their annual report.